What is GST?

Goods & Services Tax Law in India is a comprehensive, multi-stage, destination-based tax that will be levied on every value addition.

Isn’t the definition complex and confusing?

In simple words, GST is an indirect tax levied on the supply of goods and services. GST Law has replaced many indirect tax laws that previously existed in India.

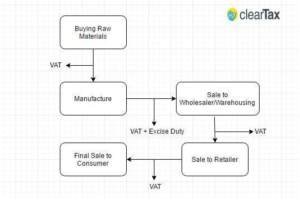

So, before GST, the pattern of tax levy was as follows:

Under the GST regime, tax will be levied at every point of sale.

Now let us try to understand “GST is a comprehensive, multi-stage, destination-based tax that will be levied on every value addition.”

Multi-stage

There are multiple change-of-hands an item goes through along its supply chain : from manufacture to final sale to consumer.

Let us consider the following case:

- Purchase of raw materials

- Production or manufacture

- Warehousing of finished goods

- Sale of the product to the retailer

- Sale to the end consumer

Goods and Services Tax will be levied on each of these stages, which makes it a multi-stage tax.

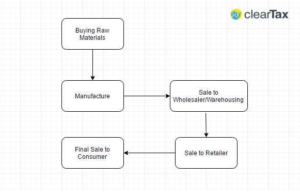

Value Addition

The manufacturer who makes shirts buys yarn. The value of yarn gets increased when the yarn is woven into a shirt.

The manufacturer then sells the shirt to the warehousing agent who attaches labels and tags to each shirt. That is another addition of value after which the warehouse sells it to the retailer.

The retailer packages each shirt separately and invests in the marketing of the shirt thus increasing its value.

GST will be levied on these value additions i.e. the monetary worth added at each stage to achieve the final sale to the end customer.

Destination-Based

Consider goods manufactured in Rajasthan and are sold to the final consumer in Karnataka. Since Goods & Service Tax (GST) is levied at the point of consumption, in this case Karnataka , the entire tax revenue will go to Karnataka.

History of GST in India

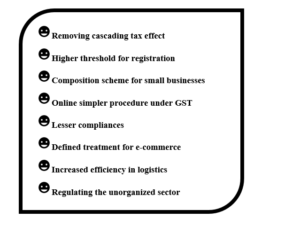

Advantages Of GST

What are the components of GST?

There are 3 applicable taxes under GST: CGST, SGST & IGST.

- CGST: Collected by the Central Government on an intra-state sale (Eg: Within Karnataka)

- SGST: Collected by the State Government on an intra-state sale (Eg: Within Karnataka)

- IGST: Collected by the Central Government for inter-state sale (Eg: Karnataka to Tamil Nadu)

In most cases, the tax structure under the new regime will be as follows:

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment